The expense to borrow money revealed as an annual percentage. For home mortgage loans, leaving out house equity lines of credit, it includes the interest rate plus other charges or fees. For house equity lines, the APR is simply the rate of interest.

A lot of elements go into choosing your home mortgage rateThings like credit rating are hugeAs are down payment, residential or commercial property type, and deal typeAlong with any points you're paying to obtain said rateThe state of the economy will also enter into playIf you do a web look for "" you'll likely see a list of interest rates from a variety of different banks and loan providers.

Should not you know how loan providers create them aruba timeshare rentals before you begin purchasing a mortgage and purchasing genuine estate?Simply put, the more you understand, the better you'll be able to negotiate! Or call out the nonsenseMany house owners tend to simply support whatever their bank or mortgage broker puts in front of them, often without researching home loan loan provider rates or asking about how all of it works.

Among the most essential aspects to effectively getting a home mortgage is securing a low rates of interest. After all, the lower the rate, the lower the mortgage payment monthly. And if your loan term lasts for 360 months, you're going to desire a lower payment. If you don't think me, plug some rates into a mortgage calculator.

125% (eighth percent) or. 25% (quarter percent) might suggest countless dollars in cost savings or costs each year. And a lot more over the whole term of the loan. Home loan rates are typically offered in eighthsIf it's not a whole number like 4% or 5% Anticipate something like 4. 125% or 5.

99% Something I 'd like to point out initially is that mortgage rates of interest move in eighths. To put it simply, when you're eventually used a rate, it will either be an entire number, such as 5%, or 5. 125%, 5. 25%, 5. 375%, 5. 5%, 5. 625%, 5. 75%, or 5.

The Best Strategy To Use For How Much Do Mortgages Cost Per Month

The next stop after that is 6%, then the process repeats itself. When you see rates advertised that have a funky percentage, something like 4. 86%, that's the APR, which factors in some of the expenses of obtaining the loan. Very same opts for essential promo rates like 4. 99% or 5.

Those popular surveys also use average rates, which don't tend to fall on the nearest eighth of a portion point. Again, these are averages, and not what you 'd in fact receive. Your actual mortgage rate will be a whole number, like 5% or 6%, or fractional, with some variety of eighths included.

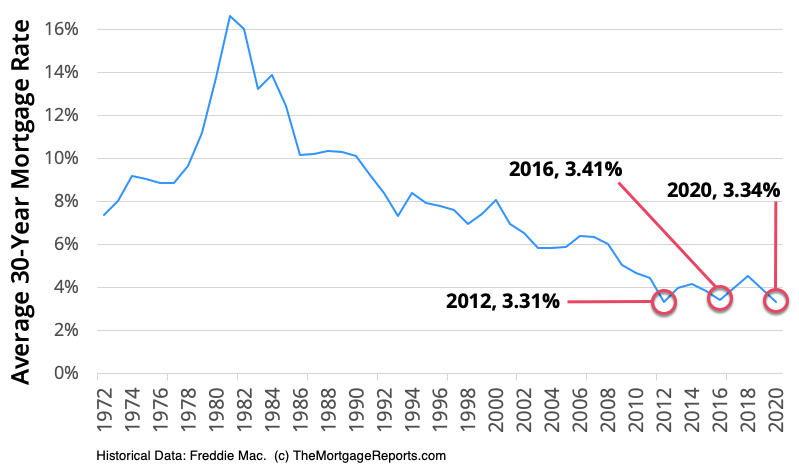

However, there are some lending institutions that might use a promotional rate such as 4. 99% rather of 5% since it sounds a lot betterdoesn't it?Either way, when utilizing loan calculators make certain to timeshare resale companies under investigation input the correct rate to guarantee precision. There are a range of elements, consisting of the state of the economyRelated bond yields like the 10-year TreasuryAnd lender and investor hunger for MBSAlong with borrower/property-specific loan attributesAlthough there are a variety of different factors that affect interest rates, the motion of the 10-year Treasury bond yield is said to be the best indication to identify whether home loan rates will increase or fall.

Treasuries are likewise backed by the "complete faith and credit" of the United States, making them the benchmark for numerous other bonds too. [Home mortgage rates vs. house prices] In Addition, 10-year Treasury bonds, also referred to as Intermediate Term Bonds, and long-term set home mortgages, which are packaged into mortgage-backed securities (MBS), compete for the exact same investors because they are relatively comparable monetary instruments.

An easy way to think the instructions of home mortgage ratesIs to take a look at the yield on the 10-year TreasuryIf it goes up, expect mortgage rates to riseIf it goes down, expect home loan rates to dropTypically, when bond rates (likewise referred to as the bond yield) increase, rates of interest go up too.

Don't confuse this with, which have an inverse relationship with rate of interest. Financiers rely on bonds as a safe financial investment when the economic outlook is poor. When purchases of bonds increase, the associated yield falls, therefore do home loan rates. But when the economy is anticipated to do well, financiers jump into stocks, forcing bond rates lower and pushing the yield (and rates of interest) greater.

The Best Strategy To Use For How Do Banks Make Money On Reverse Mortgages

You can find it on finance sites together with other stock tickers, or in the newspaper. If it's moving higher, home mortgage rates most likely are too. how do down payments work on mortgages. If it's dropping, home mortgage rates may be improving as well. To get an idea of where 30-year repaired rates will be, utilize a spread of about 170 basis points, or 1.

This spread accounts for the increased danger connected with a mortgage vs. a bond. So a 10-yr bond yield of 4. 00% plus the 170 basis points would put mortgage rates around 5. 70%. Obviously, this spread can and will vary gradually, and is actually just a fast method to ballpark home mortgage rate of interest.

So just since the 10-year bond yield rises 20 basis points (0. 20%) does not mean home loan rates will do the exact same. In reality, mortgage rates might rise 25 basis points, or just 10 bps, depending upon other market aspects. Watch on the economy also to figure out directionIf things are humming along, home loan rates might riseIf there's worry and misery, low rates might be the silver liningThis all involves inflationMortgage interest rates are really prone to economic activity, similar to treasuries and other bonds.

unemployment] As a rule of thumb, bad economic news brings with it lower home mortgage rates, and great financial news forces rates greater. Remember, if things aren't looking too hot, financiers will offer stocks and turn to bonds, and that indicates lower yields and rate of interest. If the stock market is rising, home loan rates most likely will be too, seeing that both get on positive financial news.

When they launch "Fed Minutes" or change the Federal Funds Rate, home mortgage rates can swing up or down depending upon what their report shows about the economy. Usually, a growing economy (inflation) causes greater mortgage rates and a slowing economy leads to lower home mortgage rates. Inflation also considerably effects home loan rates.

If loan originations skyrocket in a given time period, the supply of mortgage-backed securities (MBS) might increase beyond the associated need, and prices will need to drop to become attractive to buyers. This means the yield will increase, thus pressing mortgage rates of interest higher. In other words, if MBS rates go up, mortgage rates must fall.

Some Known Details About How Do Mortgages Work In The Us

But if there is a purchaser with a healthy cravings, such as the Fed, who is scooping up all the mortgage-backed securities like insane, the rate will increase, and timeshare calendar 2017 the yield will drop, thus pushing rates lower. This is why today's home loan rates are so low. Put simply, if lending institutions can offer their home mortgages for more cash, they can use a lower interest rate.